Tuesday, January 17, 2023

Monday, January 16, 2023

Monday, January 3, 2022

How Much Do You Need for Your Down Payment?

As you set out on your homebuying journey, you likely have a plan in place, and you’re working on saving for your purchase. But do you know how much you actually need for your down payment?

If you think you have to put 20% down, you may have set your goal based on a common misconception. Freddie Mac says:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

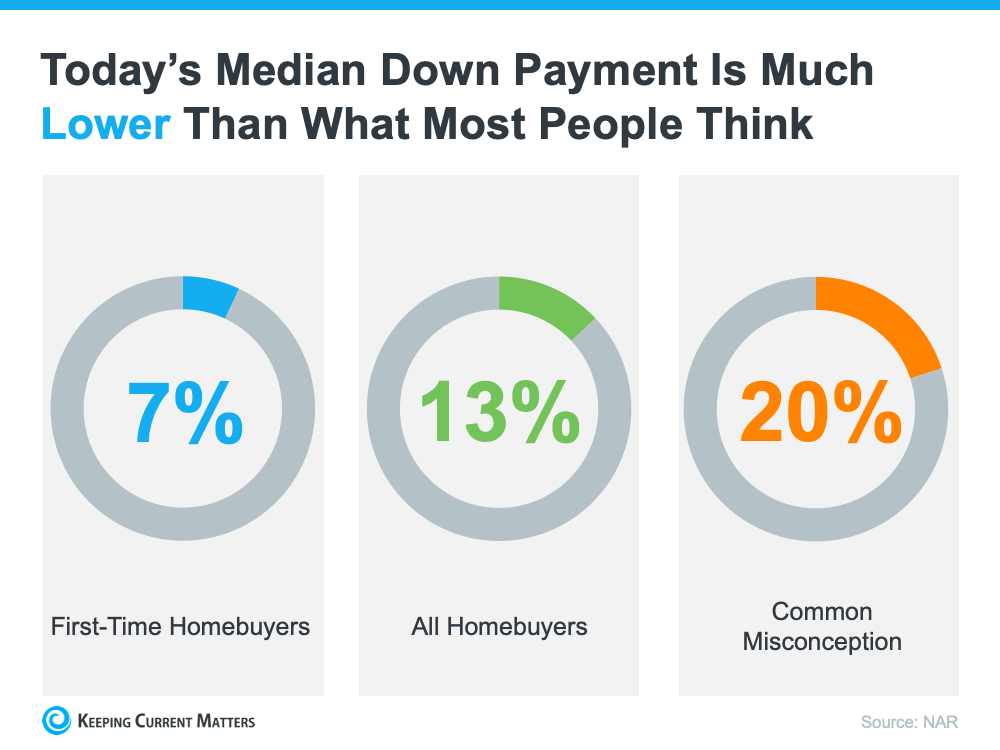

Unless specified by your loan type or lender, it’s typically not required to put 20% down. According to the Profile of Home Buyers and Sellers from the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. It may sound surprising, but today, that number is only 13%. And it’s even lower for first-time homebuyers, whose median down payment is only 7% (see graph below):

What Does This Mean for You?

While a down payment of 20% or more does have benefits, the typical buyer is putting far less down. That’s good news for you because it means you could be closer to your homebuying dream than you realize.

If you’re interested in learning more about low down payment options, there are several places to go. There are programs for qualified buyers with down payments as low as 3.5%. There are also options like VA loans and USDA loans with no down payment requirements for qualified applicants.

To understand your options, you need to do your homework. If you’re interested in learning more about down payment assistance programs, information is available through sites like downpaymentresource.com. Be sure to also work with a real estate advisor from the start to learn what you may qualify for in the homebuying process.

Bottom Line

Remember: a 20% down payment isn’t always required. If you want to purchase a home this year, reach out to a trusted real estate professional to start the conversation and explore your down payment options.

Monday, November 15, 2021

4 Things Every Renter Needs To Consider

As a renter, you’re constantly faced with the same dilemma: keep renting for another year or purchase a home? Your answer depends on your current situation and future plans, but there are a number of benefits to homeownership every renter needs to consider.

Here are a few things you should think about before you settle on renting for another year.

1. Rents Are Rising Quickly

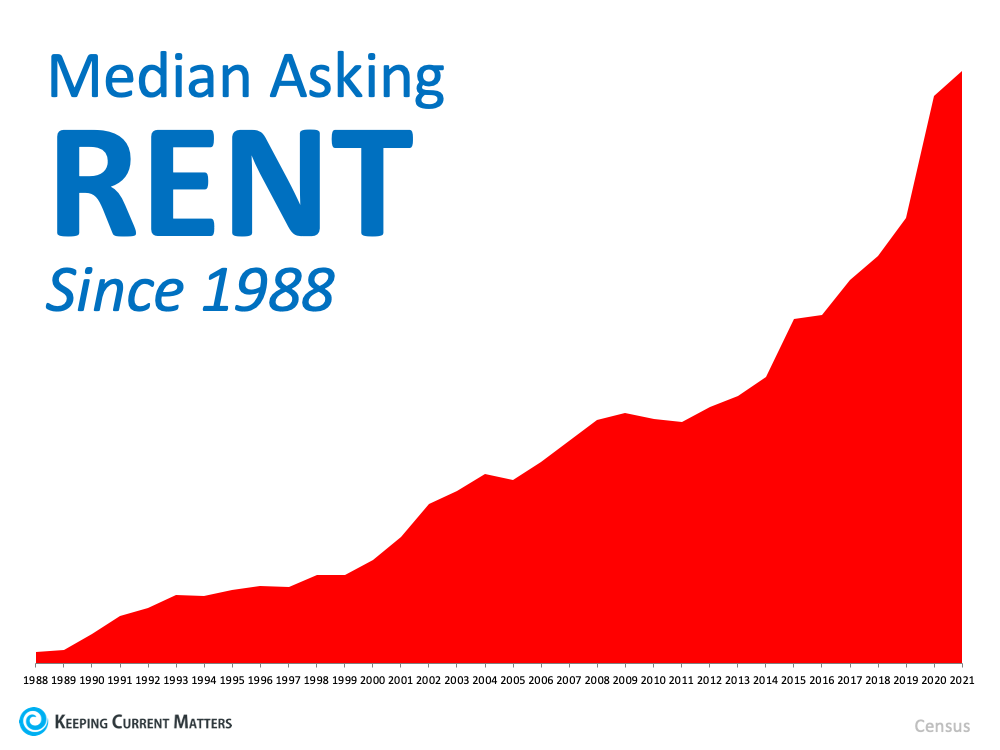

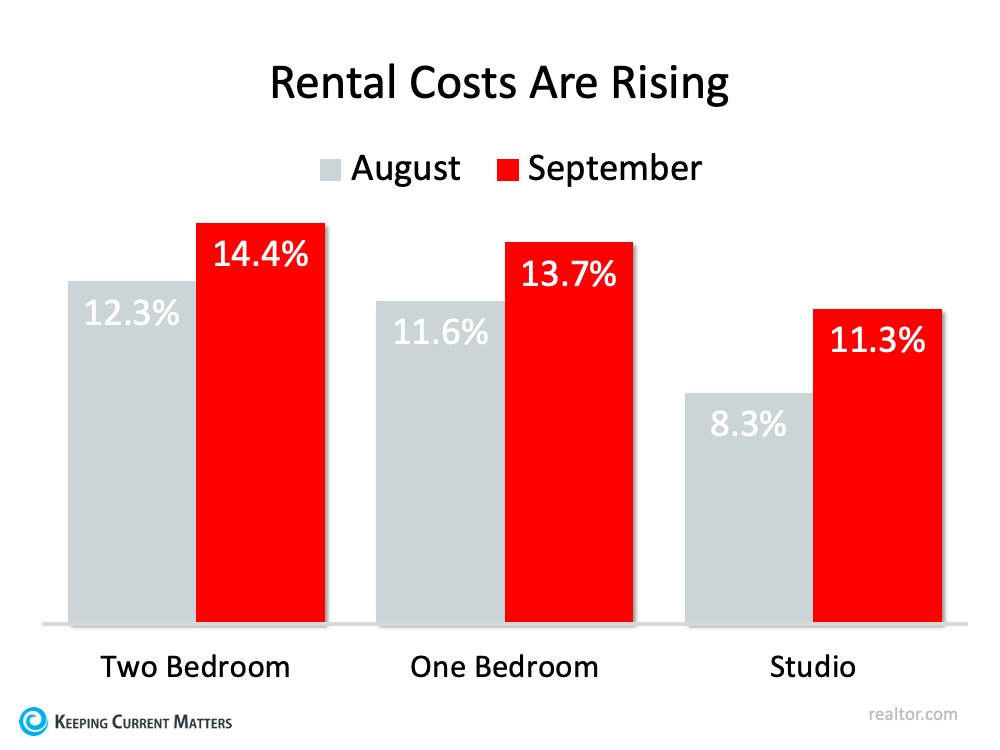

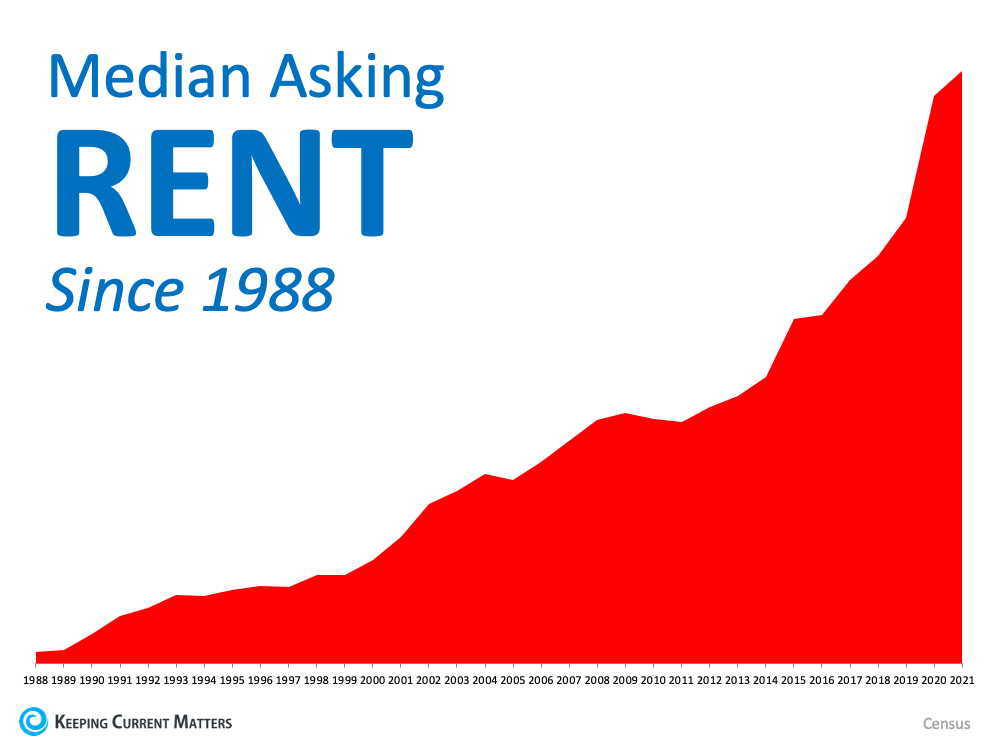

Rent increasing each year isn’t new. Looking back at Census data confirms rental prices have gone up consistently for decades (see graph below): If you’re a renter, you’re faced with payments that continue to climb each year. Realtor.com recently shared the September Rental Report, and it shows price increases accelerating from August to September (see graph below):

If you’re a renter, you’re faced with payments that continue to climb each year. Realtor.com recently shared the September Rental Report, and it shows price increases accelerating from August to September (see graph below): As the graph shows, rents are still on the rise. It’s important to keep this in mind when the time comes for you to sign a new lease, as your monthly rental payment may increase substantially when you do.

As the graph shows, rents are still on the rise. It’s important to keep this in mind when the time comes for you to sign a new lease, as your monthly rental payment may increase substantially when you do.

2. Renters Miss Out on Equity Gains

One of the most significant advantages of buying a home is the wealth you build through equity. This year alone, homeowners gained a substantial amount of equity, which, in turn, grew their net worth. As a renter, you miss out on this wealth-building tool that can be used to fund your retirement, buy a bigger home, downsize, or even achieve personal goals like paying for an education or starting a new business.

3. Homeowners Can Customize to Their Heart’s Content

This is a big decision-making point if you want to be able to paint, renovate, and make home upgrades. In many cases, your property owner determines these selections and prefers you don’t alter them as a renter. As a homeowner, you have the freedom to decorate and personalize your home to truly make it your own.

4. Owning a Home May Provide Greater Mobility than You Think

You may choose to rent because you feel it provides greater flexibility if you need to move for any reason. While it’s true that selling a home may take more time than finding a new rental, it’s important to note how quickly houses are selling in today’s market. According to the National Association of Realtors (NAR), the average home is only on the market for 17 days. That means you may have more flexibility than you think if you need to relocate as a homeowner.

Bottom Line

Deciding if it’s the right time for you to buy is a personal decision, and the timing is different for everyone. However, if you’d like to learn more about the benefits of homeownership, contact a local real estate professional. They can help you make a confident, informed decision and be your trusted advisor along the way.

Monday, November 8, 2021

Two Graphs That Show Why You Shouldn’t Be Upset About 3% Mortgage Rates

With the average 30-year fixed mortgage rate from Freddie Mac climbing above 3%, rising rates are one of the topics dominating the discussion in the housing market today. And since experts project rates will rise further in the coming months, that conversation isn’t going away any time soon.

But as a homebuyer, what do rates above 3% really mean?

Today’s Average Mortgage Rate Still Presents Buyers with a Great Opportunity

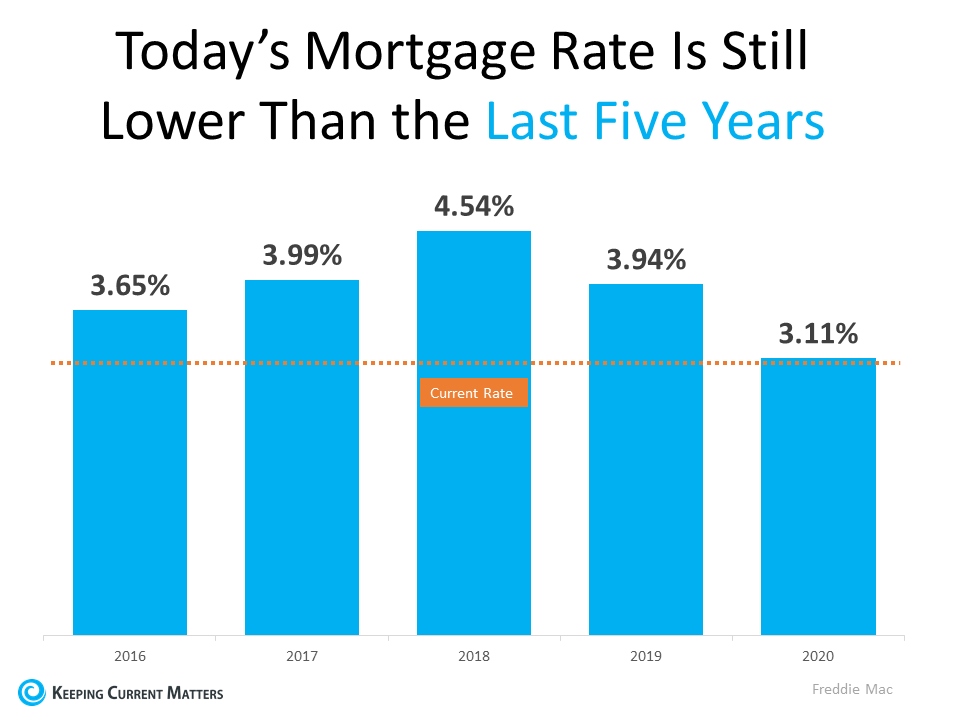

Buyers don’t want mortgage rates to rise, as any upward movement increases your monthly mortgage payment. But it’s important to put today’s average mortgage rate into perspective. The graph below shows today’s rate in comparison to average rates over the last five years: As the graph shows, even though today’s rate is above 3%, it’s still incredibly competitive.

As the graph shows, even though today’s rate is above 3%, it’s still incredibly competitive.

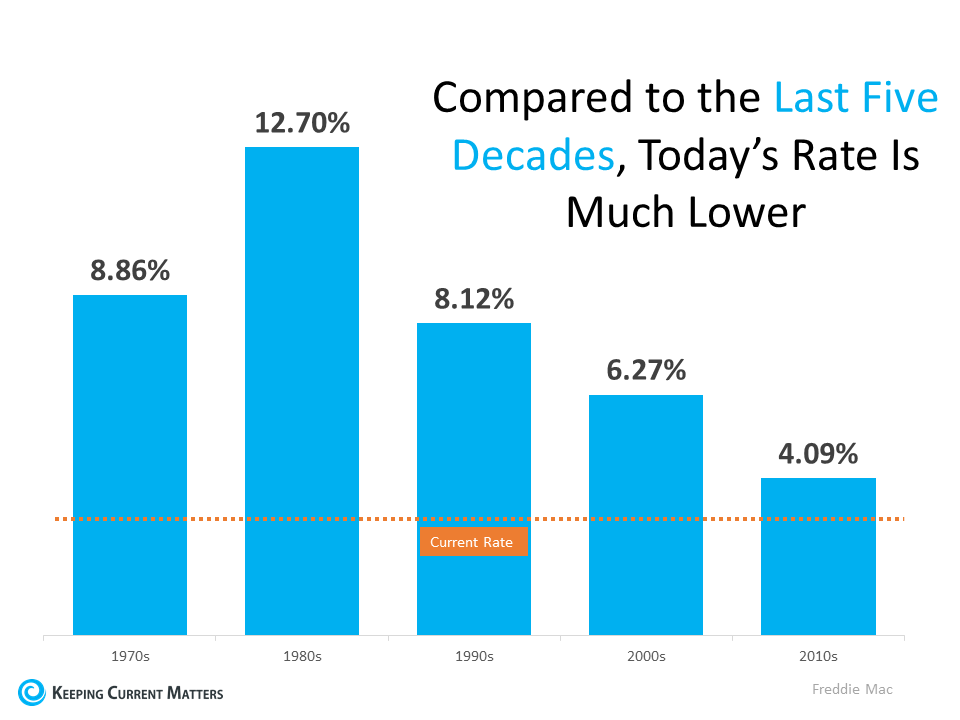

But today’s rate isn’t just low when compared to the most recent years. To truly put today into perspective, let’s look at the last 50 years (see graph below): When we look back even further, we can see that today’s rate is truly outstanding by comparison.

When we look back even further, we can see that today’s rate is truly outstanding by comparison.

What Does That Mean for You?

Being upset that you missed out on sub-3% mortgage rates is understandable. But it’s important to realize, buying now still makes sense as experts project rates will continue to rise. And as rates rise, it will cost more to purchase a home.

As Mark Fleming, Chief Economist at First American, explains:

“Rising mortgage rates, all else equal, will diminish house-buying power, meaning it will cost more per month for a borrower to buy ‘their same home.’”

In other words, the longer you wait, the more it will cost you.

Bottom Line

While it’s true today’s average mortgage rate is higher than just a few months ago, 3% mortgage rates shouldn’t deter you from your homebuying goals. Historically, today’s rate is still low. And since rates are expected to continue rising, buying now could save you money in the long run. Contact a local real estate professional so you can lock in a great rate now.

Tuesday, November 2, 2021

Renters Missed Out on $51,500 This Past Year

Rents have increased significantly this year. The latest National Rent Report from Apartmentlist.com shows rents are rising at a rate much higher than the three years leading up to the pandemic:

“Since January of this year, the national median rent has increased by a staggering 16.4 percent. To put that in context, rent growth from January to September averaged just 3.4 percent in the pre-pandemic years from 2017-2019.”

Looking back, we can see rents rising isn’t new. The median rental price has increased consistently over the past 33 years (see graph below): If you’re thinking of renting for another year, consider that rents will likely be even higher next year. But that alone doesn’t paint the picture of the true cost of renting.

If you’re thinking of renting for another year, consider that rents will likely be even higher next year. But that alone doesn’t paint the picture of the true cost of renting.

The Money Renters Stand To Lose This Year

A homeowner’s monthly mortgage payment pays for their shelter, but it also acts as an investment. That investment grows in the form of equity as a homeowner makes their mortgage payment each month to pay down what they owe on their home loan. Their equity gets an additional boost from home price appreciation, which is at near-record levels this year.

The latest Homeowner Equity Insights report from CoreLogic found homeowners gained significant wealth through their home equity this past year. The research shows:

“. . . the average homeowner gained approximately $51,500 in equity during the past year.”

As a renter, you don’t get the same benefit. Your rent payment only covers the cost of shelter and any included amenities. None of your monthly rent payments come back to you as an investment. That means, by renting this year, you likely paid more in rent than you did in the previous year, and you also missed out on the potential wealth gain of $51,500 you could have had by owning your own home.

Bottom Line

When deciding whether you should rent or buy in the future, keep in mind how much renting can cost you. Another year of renting is another year you’ll pay rising rents and miss out on building your wealth through home equity. Connect with a trusted real estate advisor today to talk more about the benefits of buying over renting.

Sunday, January 24, 2021

MARKET FOCUS: STIMULUS, SERVICE SECTOR, AND BLOCKBUSTER HOME SALES

Stocks opened lower this morning after generally unchanged yesterday. Investors are pausing to get more specifics from the Biden administration. Equity markets will love the increased spending, but how much love is where markets are today.

Biden wants a $1.9 trillion stimulus package to shorten the economic decline. Most world leaders are taking a more conservative outlook. Hopes that activity can return to normal in the hardest-hit economies are becoming increasingly distant despite the progress being made on vaccinations. U.K. Prime Minister Boris Johnson signaled that the country's current lockdown could last until the summer while officials there have suggested paying people who test positive for the virus to stay at home. German Chancellor Angela Merkel said it would be late September before everyone who wants to get vaccinated can get a shot. Anger is rising across Europe as the supply of Pfizer vaccines slows. In the U.S., President Biden will sign executive actions today that will boost food assistance for impoverished Americans.

The damage being done to economic activity was laid clear in this morning's Purchasing Managers Index numbers from Europe, which clearly signaled a double-dip recession in the euro area. IHS Markit's gauge of private-sector activity fell to 47.5, with the service sector continuing to lag, while manufacturing in Germany remained strong. Output in the U.K. fell at the quickest pace since May, with Brexit delays adding to the pandemic-driven slowdown. The ECB's survey of professional forecasters expects 2021 growth of 4.4%, down from the previous forecast for growth of 5.7%.

At 9:30 am ET, the DJIA opened -178, NASDAQ -47, S&P -17. 10 yr 1.09% -2 bp. FNMA 2.0 30 yr coupon +6 bp, -8 bp from 9:30 yesterday. 2.5 FNMA coupon +12 bp, -4 bp from 9:30 am yesterday.

At 9:45 am ET, Dec PMI expected at 55.5 as released 58.0; services PMI expected at 53.8 increased to 57.5. The strength is much stronger than in Europe.

At 10:00 am ET, Dec existing home sales were thought to be 6.550, as released +0.7%.